Glaucoma Market Share, Size, Trends, Industry Analysis Report, By Drug Class (Prostaglandin Analogs, Beta-blockers, Adrenergic Agonists, Carbonic Anhydrase Inhibitors); By Distribution Channel; By Disease Type; By Region; Segment Forecast, 2022 - 2030

- Published Date:Oct-2022

- Pages: 101

- Format: PDF

- Report ID: PM1366

- Base Year: 2021

- Historical Data: 2018-2020

Report Summary

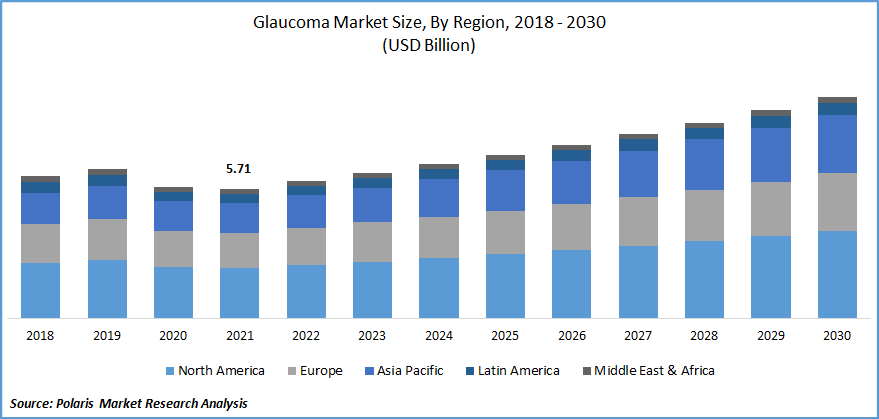

The global glaucoma market was valued at USD 5.71 billion in 2021 and is expected to grow at a CAGR of 6.2% during the forecast period. Increasing incidence rate and growing preference for cutting-edge therapeutic strategies are two of the key drivers of market expansion. According to the World Glaucoma Association, the disease will affect 79.6 million people worldwide in 2020. In 2040, there will probably be 111.8 million people in the world.

Know more about this report: Request for sample pages

One of the most prevalent ocular conditions seen in secondary and primary care settings, glaucoma is the third most common cause of blindness in the general population. According to the Bright Focus Foundation, in the United States, glaucoma affects 3 million people, 2.7 million of whom are over 40.

Over 40s in America: 3.3 million people are blind or have limited eyesight. Globally, the disease affects over 80 million individuals as of 2020, and by 2040, that figure is projected to rise to about 111 million. The pool of elderly people is growing, and the diagnosis tools are improving, helping the industry expand.

One of the key driving forces behind the positive outlook for the glaucoma market is the ongoing technological improvements in the ophthalmology sector. The desire for cutting-edge surgical techniques will drive industry expansion. The popularity of optometrists will also increase as a result of developments in medical imaging, optical coherence tomography (OCT), microinvasive glaucoma surgery (MIGS), selective laser trabeculoplasty (SLT), and progression analysis software. The market size will also increase by incorporating laser therapies as first-line therapies and medications to treat glaucoma.

Due to the implementation of preventive lockdowns in various economies, the COVID-19 pandemic negatively affected the sales of glaucoma treatments. In addition, due to a lack of healthcare infrastructure, COVID-19 patients were given priority, and all available resources were mobilized.

Additionally, many ophthalmology clinics were turned into COVID-19 wards, which limited the ability to follow up with the patients. Further, the market demand has decreased due to fewer patients visiting clinical settings since older persons are afraid of contracting an illness. However, telemedicine platforms during the epidemic enabled patients to access care promptly, which fueled industry expansion generally.

Know more about this report: Request for sample pages

Industry Dynamics

Growth Drivers

Many pipeline treatments for the disease are currently being developed, which is the key factor boosting the market growth over the forecast period. The Department of Medicinal Chemistry and the Institute for Therapeutics Discovery & Development (ITDD) at the University of Minnesota College of Pharmacy worked together to develop a novel medicine for the treatment of glaucoma.

The group created the medication QLS-101, a brand-new prodrug of the KATP connection opener levcromakalim intended to decrease the patients' episcleral vascular resistance. QLS-101 was granted a Qlaris Bio license in 2019 and has started its phase I/II clinical trials.

Further, in April 2022, Skye Bioscience appointed CMAX Clinical Research to conduct a Phase I trial for SBI-100 Ophthalmic Emulsion. CMAX, one of the world's most prominent trial operators focusing on early-phase trials, will assist Skye with subject recruitment and administering the trial medication to healthy volunteers. Thus, the launches of products and clinical trial products boost the glaucoma market growth over the forecast period.

Report Segmentation

The market is primarily segmented based on drug class, distribution channel, disease type, and region.

|

By Drug Class |

By Distribution Channel |

By Disease Type |

By Region |

|

|

|

|

Know more about this report: Request for sample pages

Prostaglandin analogs segment is expected to witness fastest growth

Segmental demand will increase due to the widespread use of prostaglandin analogs to treat the disease, which has various benefits, including only one daily dose effectiveness. Furthermore, it is projected that the segment will experience a tremendous increase due to the rising demand for prostaglandin medicines used in combination therapy.

Because it is effective at lowering intraocular pressure (IOP) and has fewer side effects than other treatments, the prostaglandin analogs sector held the largest market share for the medicines. Further divisions of the prostaglandins section include latanoprost, bimatoprost, travoprost, and others. In some rare circumstances, combination medications are another emerging therapy for treating complex and quickly developing glaucoma.

The utilization of this medication class among glaucoma patients has changed as a result of an increase in research on prostaglandin analogs. The pharmacological class offers greater efficacy and fewer side effects than other therapeutic goods and treatment choices. Improvements in glaucoma devices, however, might hurt this pattern.

Open-angle segment industry accounted for the highest market share in 2021

The open-angle disease type segment dominated the market, and it is anticipated that it will hold that position during the projected period. The disorder's high prevalence explains this compared to the other kinds of glaucoma.

Additionally, the vast majority of therapeutic medications now on the market are designed to treat open-angle type, making it the category's dominant subcategory. Additionally, increasing the use of hypotensive drugs to lower intraocular pressure is a factor in segmental growth overall.

Hospital is expected to hold the significant revenue share

Hospital pharmacies are anticipated to be the market segment with the biggest share throughout the forecast period. The significant growth is attributable to the wide availability of items for various treatment modalities.

Additionally, patients' preference for hospital pharmacies while purchasing prescription goods aids income generation. Additionally, the provision of insurance coverage and payment rules for prescription purchases made in hospital settings will improve market projections.

The demand in North America is expected to witness significant growth

Some key reasons for North America's dominance in this industry include its well-developed hospital infrastructure for diagnosis and its effective treatment framework. Since the condition progresses gradually, effective diagnostic tools enable its prompt discovery. The rising FDA approvals and drug launches for the treatment in the region are bolstering the growth.

In September 2020, the two glaucoma treatments introduced by Micro Labs USA were dorzolamide 2% and dorzolamide-timolol. Micro Labs USA plans to release new ophthalmic products in stages of FDA evaluation and development to meet the expanding demand.

Further, in July 2019, Allergan Plc reported that the New Drug Application (NDA) for Bimatoprost Sustained-Release had been approved by the US Food and Drug Administration (FDA). Bimatoprost SR would be the first-ever prolonged, reversible implant for treating individuals with primary open-angle glaucoma or ophthalmic hypertension.

According to estimates, the favorable reimbursement scenario in Europe will promote the use of glaucoma treatments. Glaucoma therapies are now part of the list of authorized, subsidized therapeutic goods available to UK citizens under the National Health Services (NHS).

In contrast, Asia Pacific is anticipated to develop at the greatest rate in the market because of the region's growing elderly population, which is particularly prevalent in nations like China and Japan. Public spending is smaller in the Asia Pacific, and most medical procedures require out-of-pocket costs.

The eye care industry has also been underdeveloped, particularly in the Asia Pacific region's poorer nations. The largest markets are Japan and South Korea, but China will grow at the highest rate due to rising healthcare costs and accelerated economic expansion. Additionally, the availability of potent generics, particularly in countries like India, will cause the anti-glaucoma medicine volume to increase. However, compared to growing regions of Asia Pacific, Japan will have the greatest development in the surgical industry.

Competitive Insight

Some of the major players operating in the global glaucoma market include Allergan PLC, Aristo Pharmaceuticals Pvt. Ltd., Aerie Pharmaceuticals Company, Akorn operating company LLC, Bausch & Lomb Incorporated, Cipla Incorporation, Fera Pharmaceuticals, LLC, Inotek Pharmaceuticals, Merck KGaA, Novartis AG, Pfizer Incorporation, Santen Pharmaceutical Co., Ltd., Teva Pharmaceutical Industries Ltd., and Valeant Pharmaceuticals International, Inc.

Recent Developments

In June 2022, the FDA approved the revised New Drug Application (NDA) for STN1011700/DE-117 (omidenepag isopropyl), which is used to treat glaucoma, according to a statement from Santen Pharmaceutical Co., Ltd., and UBE Corporation.

In March 2021, The US Food and Drug Administration has approved Teva Pharmaceuticals USA, Inc. to market the first generic version of AZOPT® (brinzolamide ophthalmic solution) 1%, a medication used to treat open-angle glaucoma and high intraocular pressure. This has extended the company's product portfolio.

Glaucoma Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2021 |

USD 5.71 billion |

|

Revenue forecast in 2030 |

USD 9.77 billion |

|

CAGR |

6.2% from 2022 - 2030 |

|

Base year |

2021 |

|

Historical data |

2018 - 2020 |

|

Forecast period |

2022 - 2030 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2022 to 2030 |

|

Segments Covered |

By Drug Class, By Distribution Channel, By Disease Type, By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

|

Key Companies |

Allergan PLC, Aristo Pharmaceuticals Pvt. Ltd., Aerie Pharmaceuticals Company, Akorn operating company LLC, Bausch & Lomb Incorporated, Cipla Incorporation, Fera Pharmaceuticals, LLC, Inotek Pharmaceuticals, Merck KGaA, Novartis AG, Pfizer Incorporation, Santen Pharmaceutical Co., Ltd., Teva Pharmaceutical Industries Ltd., and Valeant Pharmaceuticals International, Inc. |

License and Pricing

Purchase Report Sections

- Regional analysis

- Segmentation analysis

- Industry outlook

- Competitive landscape

Connect with experts

Suggested Report

- Cryptocurrency Market Share, Size, Trends, Industry Analysis Report, 2022 - 2030

- Brain Implants Market Share, Size, Trends, Industry Analysis Report, 2021 - 2028

- Security Orchestration Automation and Response (SOAR) Market Share, Size, Trends, Industry Analysis Report, 2022 - 2030

- 3D Cell Culture Market Research Report, Size, Share & Forecast by 2018 - 2026

- Green Mining Market Share, Size, Trends, Industry Analysis Report, 2023 - 2032

© 2022 Polaris Market Research and Consulting. All rights reserved